In 1975, the American Dream felt tangible for most families. A single income could often support a household, buy a home, cover healthcare, and save for retirement. Fast-forward to 2025, and that dream has eroded into a nightmare of financial precarity, debt traps, and unfulfilled promises. While headlines tout GDP growth averaging 2-3% annually since the 1970s and the S&P 500 delivering about 10% compounded annual returns over the last 50 years, these metrics paint a misleading picture of success. They obscure the harsh reality: the U.S. economy is failing hardworking Americans in profound ways, prioritizing corporate profits and elite wealth over the stability and aspirations of the middle and working classes.

This isn’t just about numbers: it’s about lives. Real median household income, adjusted for inflation, has barely budged, hovering between $66,000 and $81,000 since the 1970s, while costs for essentials like housing, education, healthcare, and childcare have skyrocketed. Inequality has widened dramatically, with the top 1% capturing a disproportionate share of gains, leaving the bottom 90% in stagnation. Even President Trump’s Make America Great Again (MAGA) agenda, with its promises of tariffs, deregulation, and tax cuts, falls short, it’s more rhetoric than reform, failing to address systemic rot like unsustainable debt and unfunded liabilities that threaten future generations.

We need Free healthcare for universal access. Workforce training in emerging industries. Childcare support for working families. Income-producing asset (IPA) assistance subsidizing up to 50% of node licenses. Rural investment in infrastructure, broadband, and jobs to bridge urban-rural divides. Cost-of living relief for essentials like electricity, food, fuel, and insurance boosting discretionary income. All paid for by the profit of American industry. And an enormous infrastructure spend on a revolutionary, low cost, ECO transportation system to move passengers and freight at high-speed, and 10 new linear cities.

Income Stagnation: The Silent Killer of the American Dream

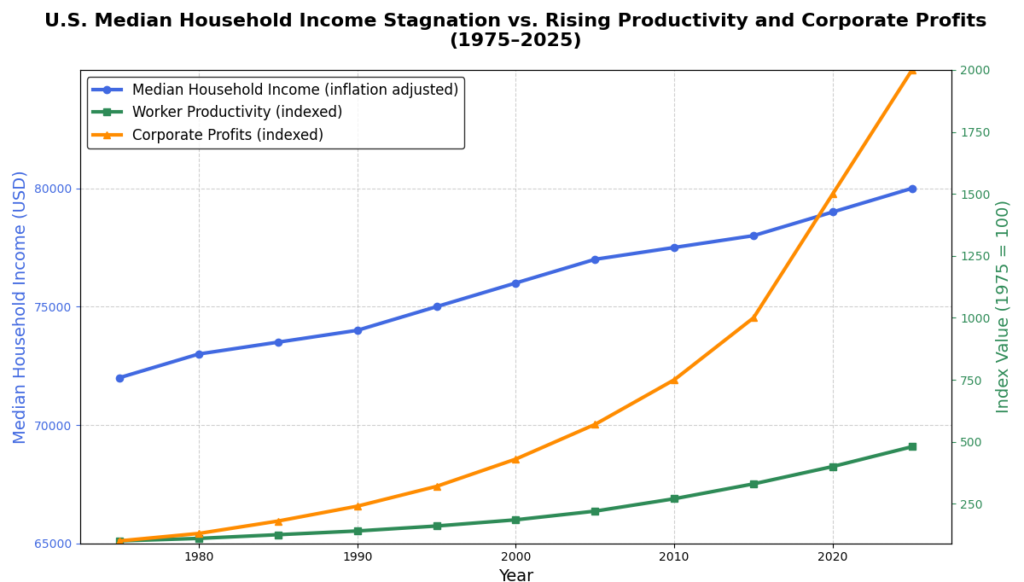

At the core of America’s economic woes is wage and income stagnation, a trend that has persisted since the mid-1970s despite surging worker productivity. Real median household income peaked at around $81,000 in 2019 but has averaged just $73,000 over the past five decades, showing minimal net growth when adjusted for inflation. This means the typical family today earns roughly what they did 50 years ago, even as the economy has expanded and corporations have reaped record profits.

- Historical Context: In the post-World War II era up to the 1970s, incomes grew robustly alongside productivity, lifting the middle class. But from 1979 to 2007, inequality siphoned off $17,867 in potential income for the broad middle class, redirecting it to the top 1%. The share of income going to the wealthiest Americans dipped in the mid-20th century but surged again starting in the 1970s, mirroring levels last seen in the Roaring Twenties.

- Modern Impacts: This stagnation has eroded upward mobility. Wages for most workers have flatlined in real terms, making families vulnerable to shocks like recessions or inflation spikes. Policies favoring globalization, union-busting, and tax cuts for the rich have exacerbated this, leaving workers with less bargaining power and more precarious jobs.

While stock market booms benefit investors, often the wealthy, ordinary Americans see little trickle-down. GDP growth masks this divide, as gains concentrate at the top, fueling a sense of betrayal among those who play by the rules but can’t get ahead.

The Housing Affordability Crisis: Homes Out of Reach for Generations

Housing, once a cornerstone of stability, has become a symbol of economic exclusion. In 1975, homeownership was attainable for most middle-class families, with prices aligned to incomes. Today, a severe shortage of over 4.5 million homes has driven affordability to crisis levels, worse than the 1980s. Nearly 75% of households can’t afford a median-priced new home in 2025, as prices have soared while incomes lag.

- Supply Shortfalls: The U.S. housing stock doubled from 36 million units in 1950 to 86million in 1980, but growth stalled post-2008 recession, leading to underbuilding amid population booms. Sun Belt cities like Phoenix and Miami, once affordable, now mimic high-cost coastal markets due to zoning restrictions and policy failures.

- Rising Costs and Barriers: Mortgage rates, though down from 18% peaks in 1981,hover around 7% in 2025, compounding high prices. This crisis stems from the 1970s onward, with deregulation and speculative investment inflating bubbles, culminating in the 2008 crash and ongoing shortages.

For families, this means delayed homeownership, higher rents (up dramatically since 1975), and generational wealth gaps. MAGA’s focus on tariffs won’t fix local zoning or corporate land hoarding—real reform demands federal incentives for affordable building and tenant protections.

Escalating Homelessness: A Stark Indicator of Systemic Failure

Homelessness, rare in the stable 1970s economy, has exploded into a humanitarian crisis, affecting over 771,000 people nightly in 2024—a 30% jump from 2022. This surge, driven by high housing costs and low wages, far exceeds historical spikes like the Great Depression or post-Civil War era.

- Trends Over Time: Modern homelessness emerged in the late 1970s with deinstitutionalization and housing cuts, but today’s scale is unprecedented, with unsheltered cases at 256,610 in 2023 (39% of total). Numbers rose from 650,000 in 2007 to current highs, tied to inequality and affordability woes.

- Broader Implications: Racial disparities persist, with people of color overrepresented, and homelessness shortens lifespans by nearly 30 years due to exposure and untreated illnesses. Economic policies ignoring root causes, like wage gaps andevictions, perpetuate this cycle.

This isn’t just a “big city” problem; it’s nationwide, eroding community stability and highlighting how GDP growth ignores human suffering.

Foreclosures and Mortgage Defaults: Cycles of Devastation

Mortgage delinquencies and foreclosures reveal ongoing instability, with rates at 1.78% in Q1 2025 (up slightly) and serious delinquencies at 0.86%. While lower than Great Recession peaks, these figures signal vulnerability in a high-rate environment.

- Historical Volatility: Rates were stable at 1-2% in the 1970s-1980s but spiked with deregulation, leading to the 2008 crisis where millions lost homes. Foreclosures hit 451,340 in 2012, dropping post-recovery but rising again to 174,100 in 2024.

- Current Pressures: High prices and rates (averaging 6.9% in 2025) strain borrowers, with delinquencies up year-over-year. This traps families in debt, delaying life milestones.

Trump’s MAGA promises economic booms, but without addressing predatory lending or affordability, foreclosures will persist as a wealth-destroying force

Credit Card Debt: The Hidden Burden of Survival

Credit card debt has surged from modest levels in the 1970s to $1.21 trillion in Q2 2025, with average per-cardholder debt at $7,321. Delinquencies reached 3.05% in Q1 2025, up from historic lows but signaling stress.

- Growth Patterns: Debt grew 5.87% yearly, far outpacing incomes, as families use cards for essentials at 20%+ APRs. Total consumer debt hit $17.57 trillion in Q3 2024, dwarfing 1970s figures.

- Consequences: This debt cycle, absent in earlier eras, leads to bankruptcies and mental strain, with delinquencies averaging 3.71% since 1991 but spiking amid inequality.

It’s a band-aid for stagnation, not prosperity, real reform must curb exploitative practices and boost wages.

Student Loan Debt: Crushing Futures Before They Begin

Student debt, under $10 billion in 1975, now exceeds $1.6 trillion, burdening 43 million borrowers. Delinquencies stand at 11.3% for federal loans, with defaults at 6.24%.

- Explosion Since 1970s: Tuition hikes (155% since 1960) and loan shifts from grantsdrove this, from $516 billion in 2008 to today. Pre-1980s, debt was minimal; now,it delays homebuying and families.

- Inequity: Minorities and low-income groups bear the brunt, perpetuating cycles of poverty.

Biden’s relief efforts face blocks, but broader fixes, like free community college, are needed beyond MAGA’s scope.

Healthcare: A Bankrupting System Undermining Security

Healthcare costs have ballooned from $353 per capita in 1970 to $14,570 in 2023, with spending at $4.9 trillion. Uninsured rates fell post-ACA, but affordability crises cause bankruptcies.

- Rising Burden: Costs quadrupled as GDP share since 1970, outpacing inflation. In the 1970s, access was better relative to costs; today, it’s a leading debt driver.

- Mental Health Tie-In: Issues affect 23.1% of adults (59.3 million in 2022), up since 1990, linked to economic stress.

This erodes savings and health, demanding universal coverage reforms.

Childcare and Food Insecurity: Barriers to Family and Basic Needs

Childcare costs rose from $233 annually in the 1960s to $13,128 in 2024, costing the economy $122 billion yearly. Food insecurity hit 13.5% of households in 2023 (47.4 million people), up from early 2000s.

- Trends: Childcare “deserts” affect half of Americans, worse than informal 1970s options. Insecurity rose with inequality, higher than pre-recession levels.

- Impacts: Forces parents out of work, deepening poverty.

Retirement Insecurity: No Safety Net for the Golden Years

Pensions shifted from defined-benefit (common in 1975) to risky 401(k)s, leaving 55% of near-retirees with under $25,000 saved. Savings rates fell from 11.7% in the 1960s-1970s to 4.4%, with a $6.8-$14 trillion deficit.

- Unfunded Liabilities: Social Security ($62.8 trillion), Medicare ($106.6 trillion), federal benefits ($15 trillion), and state pensions ($1.49 trillion) total $100–222 trillion, risking cuts.

- Fiscal Instability: The federal deficit exceeds $67,000 per American, worrying 57% (Pew 2025), with rising national debt ($36.2 trillion) threatening inflation or crisis.

This unsustainable system, amplified since the 1970s, endangers retirees.

The Looming Fiscal Cliff: Debt and Deficits Threatening Everything

Beyond daily struggles, America’s financial system is unsustainable. The national debt tops $36.2 trillion, with unfunded liabilities soaring to $100–222 trillion. The deficit per American ($67,000) alarms 57% about instability, risking inflation, dollar devaluation, or austerity.

- Rising Risks: Debt-to-GDP ratios exceed safe levels, echoing warnings from economists. This could trigger crises, eroding savings and programs.

- Why MAGA Isn’t Enough: Trump’s plans ignore these, focusing on growth without addressing inequality or liabilities.

A Call for Real Reform: Beyond Metrics and Promises

The economy’s “success” is a myth for most. GDP and stocks soar, but families face stagnation, debt, and despair unimaginable in 1975. We need comprehensive reform: progressive taxes, universal healthcare, affordable housing mandates, and strengthened social safety nets.

Get informed. Get involved. Sign the petition for economic justice here. Your voice can demand change, before it’s too late.