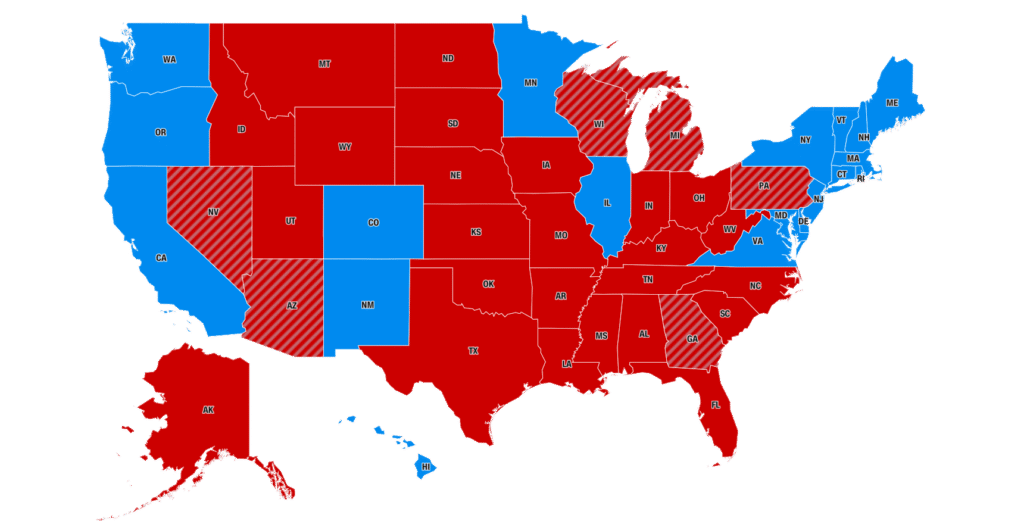

In the aftermath of the 2024 presidential election, Donald Trump emerged victorious in 31

states, capturing a broad swath of the American heartland and Sun Belt. However, beneath this

political triumph lies an economic challenge that affects millions: approximately 69% of residents

in these Trump-voting states cannot afford to purchase a median-priced home. This statistic is a

population-weighted average derived from state-specific data on median home prices, required

incomes for affordability (incorporating a 20% down payment, mortgage rates around 7%,

property taxes, and homeowners insurance), and household income distributions modeled as

lognormal with a standard deviation of 0.63.

The model is calibrated to national figures where about 73% of households are priced out, reflecting broader trends in housing unaffordability. This article examines this crisis, ranks the states from most to least affordable, identifies the primary causes, explores why voters supported Trump in hopes of relief, argues that such expectations are unrealistic due to gaps in the MAGA agenda, and introduces the American Dream Rail Legacy Project as a potential supplement. It concludes with a call to action for readers.

States Ranked: From Most to Least Affordable for Homebuyers

Affordability is assessed by the percentage of households earning less than the income needed

to keep housing costs at or below 28% of gross income, using the lognormal distribution to

estimate income spread. Data from early 2025 shows significant variation, with even the

most affordable states excluding over 30% of residents. The ranking is from lowest (best) to

highest (worst) percentage unable to afford.

- West Virginia: 30.7% – Median price $170,514; income $60,410. Low prices provide relative relief, though low wages limit access.

- Iowa: 42.3% – Median price $237,298; income $80,860. Stable Midwestern economy helps, but rising costs erode gains.

- Indiana: 43.5% – Median price $254,805; income $76,910. Industrial base keeps prices moderate.

- Kansas: 45.0% – Median price $243,092; income $84,830. Agricultural stability aids affordability.

- Ohio: 47.3% – Median price $245,994; income $73,770. Manufacturing hubs offer some balance.

- Missouri: 47.9% – Median price $264,878; income $78,290. Mixed urban-rural dynamics.

- Arkansas: 48.6% – Median price $220,174; income $63,250. Low prices, but income lags.

- Oklahoma: 50.1% – Median price $219,076; income $67,330. Energy sector volatility impacts insurance.

- Mississippi: 50.7% – Median price $190,755; income $55,060. Cheapest homes, lowest incomes.

- Michigan: 51.8% – Median price $259,483; income $76,960. Auto industry recovery helps slightly.

- Alabama: 52.5% – Median price $232,205; income $60,660. Southern low costs offset by wages.

- Pennsylvania: 52.5% – Median price $286,033; income $79,820. Energy and urban divides.

- Kentucky: 54.4% – Median price $224,934; income $61,980. Flood risks raise insurance.

- North Dakota: 55.5% – Median price $289,192; income $76,960. Oil influences prices.

- Nebraska: 55.8% – Median price $277,245; income $89,190. High incomes, moderat taxes.

- Louisiana: 60.0% – Median price $214,187; income $57,650. Hurricane-prone, high insurance.

- Alaska: 61.0% – Median price $394,781; income $98,190. Remote costs hurt despite high wages.

- South Carolina: 62.1% – Median price $307,144; income $69,100. Coastal growth drives prices.

- Wyoming: 63.7% – Median price $366,667; income $77,200. Energy and rural factors.

- Tennessee: 65.1% – Median price $336,083; income $72,700. Nashville boom inflates.

- Wisconsin: 65.3% – Median price $333,775; income $79,690. Taxes offset prices.

- South Dakota: 65.5% – Median price $321,486; income $81,740. Rural appeal, high taxes.

- Georgia: 66.7% – Median price $339,764; income $72,420. Atlanta surges demand.

- Texas: 67.5% – Median price $309,450; income $79,060. High property taxes, no income tax.

- North Carolina: 69.8% – Median price $340,100; income $68,610. Migration increases competition.

- Utah: 70.1% – Median price $547,417; income $101,200. Tech growth pushes prices.

- Arizona: 72.4% – Median price $441,802; income $82,660. Heat risks elevate insurance.

- Nevada: 73.1% – Median price $473,604; income $81,310. Tourism inflates Vegas market.

- Montana: 79.6% – Median price $468,222; income $79,220. Remote worker influx.

- Idaho: 79.8% – Median price $476,401; income $73,910. Similar migration effects.

- Florida: 83.0% – Median price $407,830; income $72,200. Hurricanes make insurance prohibitive.

This ranking highlights patterns: states with low prices and modest costs like West Virginia and

Iowa perform better, while growth and disaster-prone areas like Florida and Idaho fare worst.

The 69% average underscores how lower home prices in red states ($192 per square foot vs.

$322 in blue states) are offset by lower median incomes ($69,000 vs. $87,000), leaving many

behind.

The Top Three Contributors to the Affordability Crisis

The 69% unaffordability rate results from systemic issues, amplified in Trump-voting states by

lower incomes despite cheaper housing. Key causes include a severe housing supply shortage, high mortgage interest rates, and stagnant wages amid income inequality and rising costs, based on 2025 reports.

Severe Housing Supply Shortage

The U.S. faces a shortfall of over 4.5 million homes, stemming from post-Great Recession underbuilding and surging demand from millennials and migration. In red states, while looser regulations allow more building per capita, zoning barriers and rapid population growth (e.g., in Texas and Florida) have driven prices up 60% since 2019, with the national median at $412,500—five times median income, exceeding the affordable ratio of three. Affordable units are scarce, with a 7.3 million deficit for low-income renters, forcing competition and burdening 74% of extremely low-income households to spend over half their income on housing.

High Mortgage Interest Rates

Rates averaging 6.76% in early 2025 have elevated borrowing costs, with monthly payments on a $412,500 home reaching $2,570, requiring $126,700 in income, attainable for only 13% of renters. In lower-income Trump states, this excludes more residents, freezing the market with sales at 30-year lows. Ancillary costs compound the issue, with home insurance premiums up 57% from 2019 to 2024 and property taxes rising 12% between 2021 and 2023, particularly in disaster-prone areas like Florida and Louisiana.

Stagnant Wages and Income Inequality Relative to Rising Costs

Wages have not matched housing inflation, with the housing wage for a two-bedroom rental at $32.11 per hour—above minimums in many red states. Income inequality, modeled in the lognormal distribution, means over half of households earn below median, amplifying unaffordability. Low wage jobs dominate in red states, and post pandemic material costs add pressure.

Nationally, 50% of renters and 24% of owners are cost-burdened, with declining homeownership rates. Federal programs help only one in four eligible households, leaving red state residents underserved.

Why Voters Turned to Trump: A Belief in Solutions That May Not Materialize

Voters in these states backed Trump, believing his MAGA and America First agenda would address these factors through tax cuts, deregulation for supply, and economic growth via tariffs and energy policy. Proposals like no taxes on overtime or tips aim to boost wages, while deregulation could accelerate building in red states, and immigration controls might ease demand in growth areas like Texas. Supporters viewed this as a route to lower rates, higher incomes, and affordability.

However, this is nothing more than wishful thinking that will amount to nothing, as the MAGA plan lacks critical elements to tackle the three causes. Tax cuts may widen inequality without targeted supports, and tariffs could inflate construction costs, hindering supply. High rates depend on Federal Reserve actions, not presidential control, and America First focuses on nationalism over specific housing reforms like affordable unit incentives. Ultimately, these policies overlook the need for substantial investments in supply and income equity, leaving the 69% unaffordability unchanged.

The American Dream Rail Legacy Project: A Supplement to Fill the Gaps

The American Dream Rail Legacy Project was incepted to offer President Trump a nine-point plan that contains the very critical elements the MAGA plan is missing, serving as a supplement to enhance the America First agenda. This $5.5 trillion initiative aims to build an all-electric, high-speed rail system for 53-foot trailers at 100 mph, integrating the trucking industry to revive the fading American Dream. Its purpose is to address economic struggles like stagnant wages, high housing costs, and unaffordability by generating $9.9 trillion in GDP, empowering workers through profit-sharing, and modernizing infrastructure under a nine-point MAGA Legacy Plan. By shifting from outdated railroad monopolies to a meritocratic system, it creates jobs, promotes sustainability, reduces freight emissions by 50%, and invests in deindustrialized areas, blending trucking and rail with retraining programs.

The project’s backbone is its nine-point plan, a strategic roadmap designed to transform industries and empower Americans. Here’s a breakdown:

- Supplement the income of long-haul truck drivers to enhance financial stability: This directly tackles stagnant wages by providing additional earnings from industry profits, helping drivers afford housing amid rising costs.

- Modernize the trucking industry with blockchain for efficiency and transparency: Utilizing blockchain tokens and licenses, it creates passive income streams, turning trucks into revenue-generating nodes to democratize profits and circulate value back to workers.

- Streamline supply chain management to reduce costs and bottlenecks: By optimizing logistics through integrated rail-trucking, it lowers construction and material costs, indirectly alleviating housing supply shortages.

- Enable hardworking Americans to attain prosperity in 12 years by turning assets into blockchain nodes: This empowers individuals to build wealth rapidly, supplementing incomes so much that they can achieve debt-free homeownership in as little as twelve years through accelerated payoffs and profit dividends.

- Build an intercontinental transportation system via Dream Rail: The core infrastructure project reduces wasteful long-hauls, creates high-paying jobs, and boosts economic growth to make homes more attainable.

- Reindustrialize America to bring back high-paying jobs: Focusing on deindustrialized red states, it revives manufacturing and energy sectors, increasing wages and reducing income inequality.

- Rebuild middle-class America by transitioning workers into capitalists: Through cooperatives and asset socialization, workers become stakeholders, gaining access to industry profits to supplement stagnant wages and overcome affordability barriers.

- Ensure financial system sustainability through trade values: By promoting fair trade and blockchain-based transparency, it stabilizes the economy, potentially lowering interest rates and ancillary costs like insurance.

- Incentivize sustainable living with eco-friendly tech: Integrating green technologies cuts emissions and supports resilient housing, reducing long-term costs in disaster-prone areas.

This plan addresses housing indirectly by creating jobs and income streams that make homes more attainable, but also directly through enhanced financial stability and wealth-building mechanisms. For instance, by sharing trucking and rail profits via blockchain, workers gain thousands in annual supplements, enabling better mortgage terms and faster equity buildup. If President Trump were to embrace this nine-point plan, integrating its elements as a supplement to the MAGA plan, he would most certainly be able to substantially reduce the cost of mortgage interest—up to 70%—through profit-subsidized financing models and community investment funds. Moreover, access to industry profits would supplement stagnant wages so significantly that Americans could own their homes debt-free and clear in as little as twelve years, filling the gaps in America First by providing targeted supports for supply efficiency, wage enhancement, and rate reductions.

Call to Action: Get Informed, Get Involved, Sign the Petition

The 69% unaffordability in Trump-voting states demands urgent action beyond politics. Get

informed by exploring housing data and the American Dream Rail Legacy Project at

americandreamrail.org. Get involved by advocating to lawmakers for its adoption. Sign the

petition on the site to press Trump to embrace the nine-point plan. Collective effort can restore

the American Dream of homeownership.